11

11

Across the globe, cryptocurrency users continue to encounter significant hurdles, with bank accounts frequently being frozen and transfers blocked, a persistent issue that stands in stark contrast to the rising tide of institutional adoption. Panos Mekras, co-founder and CEO of blockchain fintech Anodos Labs, shared his early experiences with crypto in Greece during the late 2010s, a period when most Greek banks outright disallowed transfers to crypto exchanges. Mekras personally experienced blocked card payments until one bank, after extensive questioning to ensure he understood the perceived "risky" nature of his counterparty, finally permitted his transactions.

Mekras explained to Cointelegraph that these early rejections were symptomatic of a broader banking approach that viewed digital assets as inherently high-risk. This classification frequently resulted in unexplained account closures or sudden freezes, ultimately compelling his business to rely exclusively on on-chain tools and payment rails. While public perception of crypto has since evolved, transitioning from a speculative asset class to a foundational layer for future financial products, Mekras stated that he still encounters the same banking barriers, with a recent incident occurring "a few months ago." He recounted, "I tried to send money from an exchange to Revolut, and they froze my account for three weeks. I had no access to my [funds] during that time."

The Long Shadow of Crypto Debanking Persists

Mekras’s experience is far from isolated. Despite banks announcing expansions into crypto custody and blockchain initiatives, a significant number of crypto holders continue to face similar challenges. A January report from the UK Cryptoasset Business Council highlighted that bank transfers to cryptocurrency exchanges were frequently blocked or delayed. The report found that approximately 40% of payments encountered restrictions, and 80% of exchanges reported an increase in friction over the past year. The council issued a warning that blanket bans and transaction limits are often implemented without due consideration for the legal status of the exchange involved.

Revolut, the platform where Mekras experienced his recent account freeze, is noted as one of only two banks in the UK council’s study that permit both bank transfers and debit card usage for crypto-related transactions. Revolut operates as an authorized UK bank with certain restrictions, currently in the process of building out its banking infrastructure before a full launch. It also holds a European Union banking license through Lithuania and offers crypto trading services within its application.

A Revolut spokesperson informed Cointelegraph that account freezes are considered a "last-resort" measure implemented for customer protection and in compliance with Anti-Money Laundering (AML) and Know Your Customer (KYC) regulations. The spokesperson elaborated, "A temporary freeze may occur if our systems detect irregular activity. This could be a combination of a few factors, such as if a customer interacts with a platform frequently exploited by fraudsters, or we believe that the funds in question may be the proceeds of crime or sanctions circumvention." The representative also stated that since October 1st, only 0.7% of Revolut accounts with crypto deposits experienced restrictions or freezes after an investigation.

When Banks Close Doors, Users Navigate On-Chain Solutions

In certain regions, outright bans on cryptocurrency have pushed users towards more extreme measures. In countries like China, where on- and off-ramps for crypto are not legally permissible, users resort to peer-to-peer (P2P) platforms or black markets to facilitate trades. While China represents an extreme end of the spectrum, other jurisdictions have begun to ease restrictions. Nigeria, which previously banned crypto and even blocked P2P platforms, formally recognized digital assets as securities in 2025.

Similar banking friction patterns have also emerged in the United States. Lawmakers and industry participants have invoked the term "Operation Chokepoint 2.0" to describe what they allege are informal directives from federal regulators discouraging banks from maintaining relationships with cryptocurrency companies. The original "Operation Choke Point" was an initiative where enforcement agencies were accused of pressuring banks to sever ties with industries deemed politically contentious, such as payday lenders and firearms sellers.

The inauguration of Donald Trump as U.S. President in January 2025 brought a renewed push for crypto-friendly policies, aiming to position the U.S. as the "crypto capital" of the world. Following this shift, debanking issues concerning cryptocurrency have received official recognition. In December, the U.S. Office of the Comptroller of the Currency (OCC) released its findings on debanking practices by nine of the country’s largest banks. The OCC also published an interpretive letter confirming that banks are permitted to facilitate crypto transactions in a broker-like capacity. Despite this positive momentum, users continue to report that the banking sector remains reluctant to service accounts exposed to cryptocurrencies. Mekras noted, "This is still the case [and] there are still anti-crypto positions. Some have even said publicly that they are not willing to support crypto activity or engage with the industry." Mekras suggested that users could consider completely detaching from the traditional banking system and moving their finances entirely on-chain. While this may be theoretically viable, in practice, most businesses and individuals still require access to fiat rails to operate.

Banking’s Gradual Turn Towards Blockchain Infrastructure

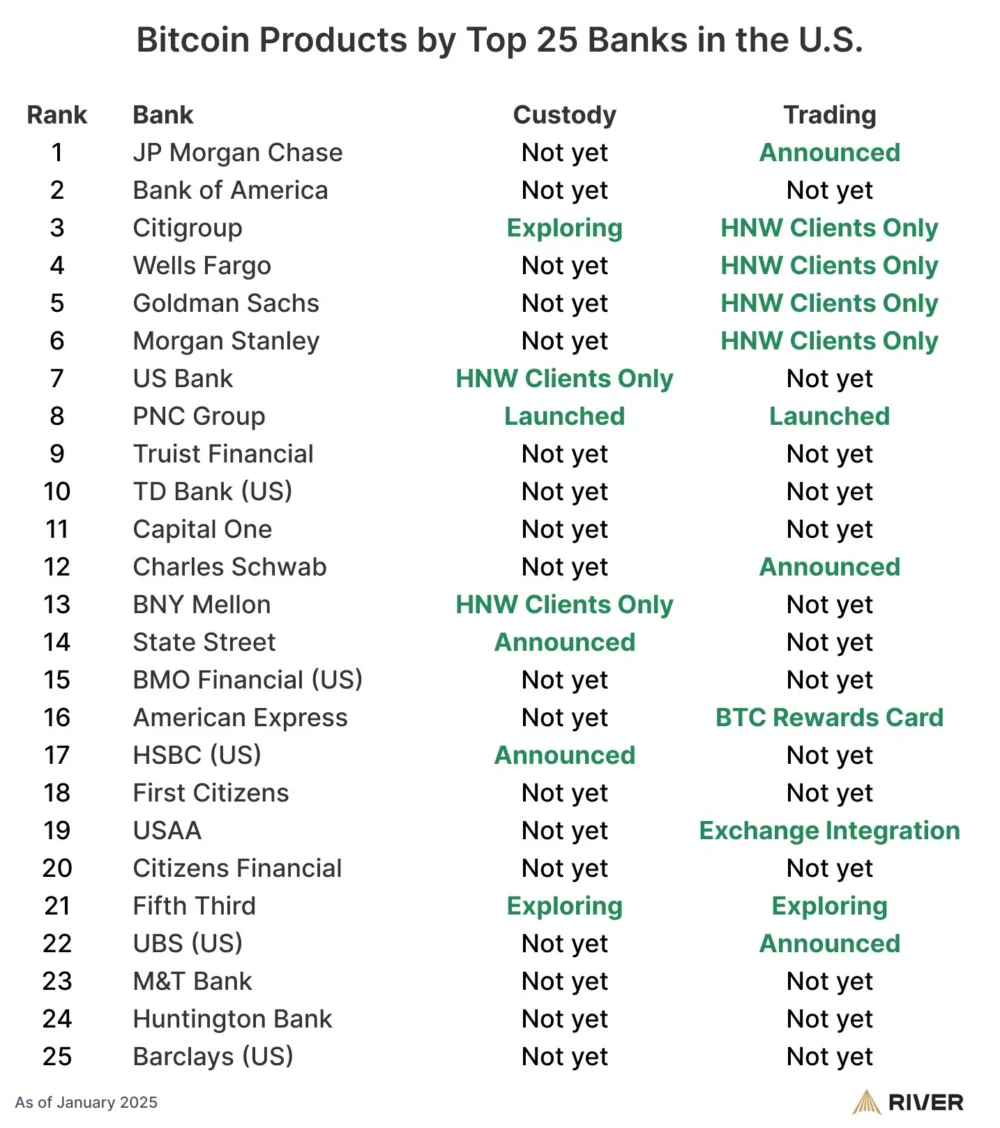

In recent years, a discernible global shift has occurred in how traditional financial institutions engage with cryptocurrency. Major banks and financial infrastructures are increasingly developing products and services that integrate with Web3. In the U.S., a reported 60% of the top 25 banks are either offering or planning to offer Bitcoin-related services, including custody, trading, and advisory solutions. Across Europe, regulated services such as crypto custody and settlement are being introduced by legacy exchanges and financial groups under the Markets in Crypto-Assets Regulations (MiCA). In the UK, HSBC’s blockchain platform was selected to support pilot issuances of tokenized government bonds.

Against this backdrop of increasing institutional adoption, some companies working to bridge the gap between traditional banking and blockchain suggest that the challenges leading to account freezes are rooted in tooling gaps and risk frameworks within banks. Eyal Daskal, CEO of Crymbo, a blockchain infrastructure platform for institutions, explained to Cointelegraph, "The problem is that there’s a huge amount of friction because traditional banks don’t really have the internal infrastructure to interpret blockchain data in a way that fits inside their existing risk and compliance frameworks." He described the situation as one where banks often resort to precautionary measures due to a lack of tools to properly assess on-chain activity and link it to identity and compliance signals. Daskal added, "If crypto is involved, they block the account and treat it as out of scope. It’s the simplest option for them because they don’t have the tools to assess it properly."

As cryptocurrency moves further into the financial mainstream, access to basic banking services for many users still hinges on whether a bank’s risk engine can interpret on-chain activity. Until this fundamental gap is bridged, the industry’s embrace by institutions and the ongoing friction faced by retail users are likely to coexist.